Imagine your prescription copay jumping from $15 to $113 overnight. For millions of Americans relying on Medicare Part D is the federal program that provides prescription drug coverage for people with Medicare, this isn't a hypothetical nightmare-it's the reality of formulary updates are systematic changes to which drugs an insurance plan covers and at what cost. These lists of covered medications shift annually, often forcing patients into generic switching is the process of replacing a brand-name drug with its generic equivalent to reduce costs without warning.

If you're navigating these changes in 2026, you need more than just a notification letter. You need a strategy. The landscape has shifted dramatically due to the Inflation Reduction Act (IRA), bringing both relief-like a hard cap on spending-and new complexities around biosimilars and negotiated drug prices. This guide breaks down exactly how these updates work, why insurers make them, and how you can protect your health and your wallet.

Why Your Drug Coverage Changes Every Year

Insurance plans don't change their formularies just to be difficult. They do it to manage risk and comply with evolving regulations. Since the inception of Medicare Part D in 2006, Pharmacy Benefit Managers (PBMs) are companies that administer prescription drug programs for health insurers and employers like OptumRx, CVS Caremark, and Express Scripts have controlled roughly 84% of the market. Their job is to negotiate prices with pharmaceutical companies.

When a patent expires on a blockbuster drug, generics enter the market. PBMs then pressure plans to switch patients to these cheaper alternatives. According to Milliman’s analysis, 78% of standalone Prescription Drug Plans (PDPs) implemented aggressive generic substitution policies for 2025. This trend continues into 2026 as the IRA eliminates rebate-driven incentives for keeping expensive brand-name drugs on formularies. Instead, plans are incentivized to steer patients toward lower-cost options to maintain profitability, which J.P. Morgan analysts project could drop by 18-22% through 2027.

For you, the patient, this means your trusted medication might suddenly move to a higher tier or get excluded entirely. Understanding that this is a structural business decision, not a personal oversight, helps you approach the problem proactively rather than reactively.

The New Rules of the Road: IRA Impact on Costs

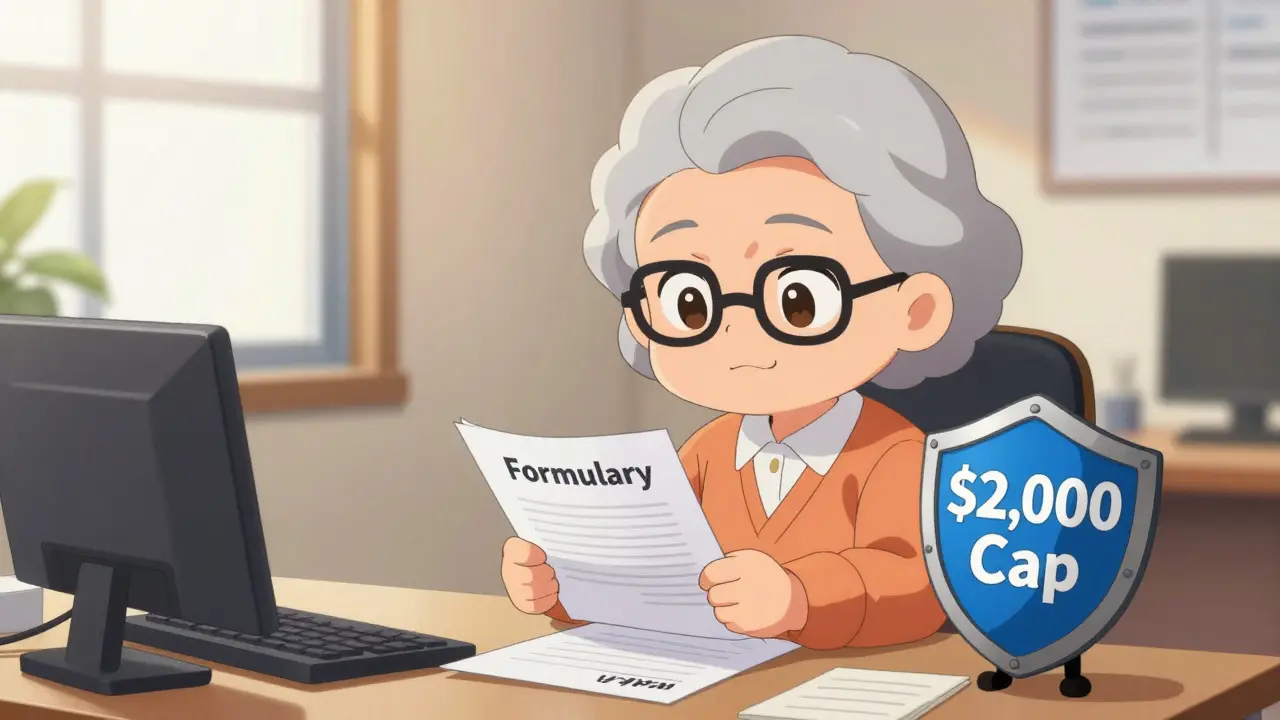

The Inflation Reduction Act, signed in 2022, fundamentally rewrote the rules for prescription drug coverage. The most significant change for patients took effect on January 1, 2025, and remains critical in 2026: the $2,000 annual out-of-pocket cap is a limit on how much Medicare Part D beneficiaries pay for prescriptions each year.

Before this cap, many seniors faced catastrophic spending, paying thousands out of pocket during the "donut hole" coverage gap. That gap is now gone. Once you hit $2,000 in true out-of-pocket costs, the plan covers 100% of your drug expenses. AARP estimates this saves an average of $1,500 per year for the 3.2 million enrollees who previously exceeded this threshold.

However, the cap doesn't mean drugs are free until you hit that number. You still face tiered copays. Here is how the typical 2026 structure looks based on CMS data:

| Tier | Drug Type | Average Copay |

|---|---|---|

| Tier 1 | Preferred Generics | $1 - $10 |

| Tier 2 | Non-Preferred Generics / Preferred Brands | $47 |

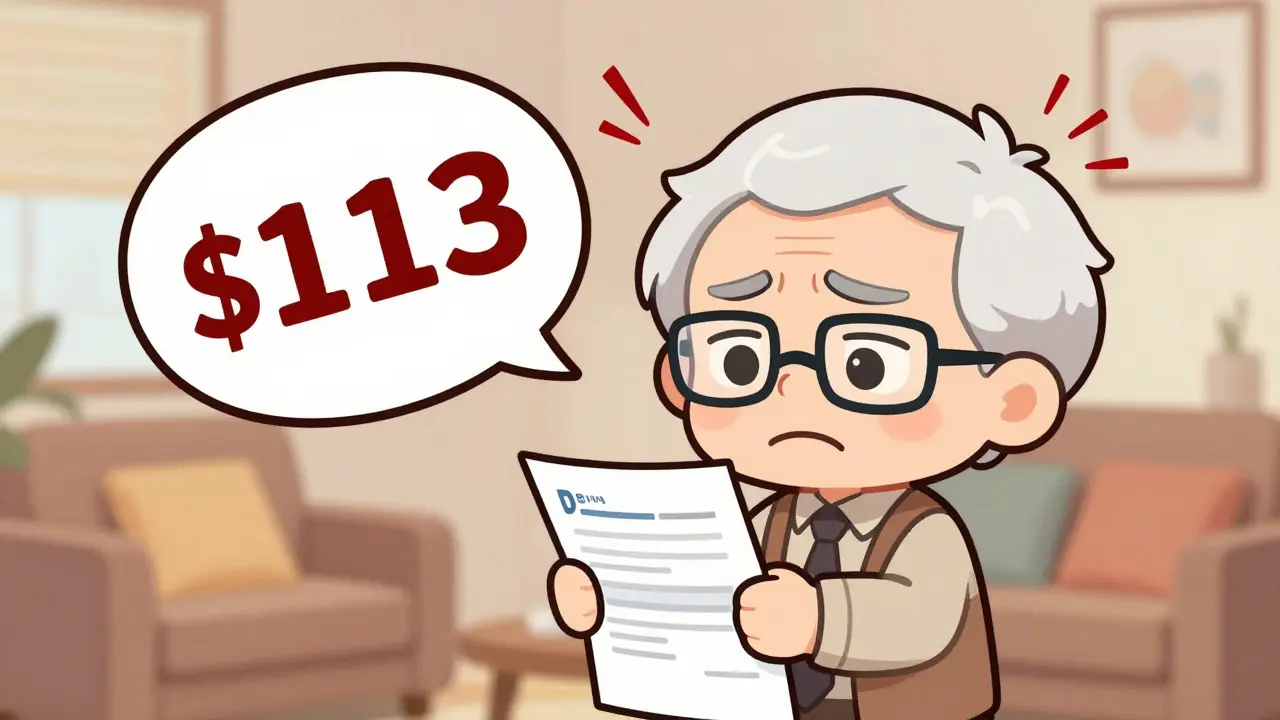

| Tier 3 | Non-Preferred Brands | $113 |

| Specialty | High-Cost Medications | $113 or 25% Coinsurance |

Notice the jump between Tier 1 and Tier 2? That’s where formulary updates hurt most. If your drug moves from Tier 1 to Tier 3, your annual cost could skyrocket, eating up that $2,000 cap quickly.

Generic Switching vs. Biosimilars: What’s the Difference?

You’ve heard of generics, but what about biosimilars? As we move deeper into 2026, biosimilars are becoming a major part of formulary strategies. While traditional generics are chemically identical copies of small-molecule drugs (like aspirin or metformin), biosimilars are highly similar versions of complex biological drugs made from living cells.

Biological drugs treat serious conditions like cancer, rheumatoid arthritis, and Crohn's disease. They are expensive to produce. When a biologic loses exclusivity, biosimilars enter the market. The FDA approved 17 biosimilars in 2024 alone, a 34% increase. By 2027, experts project biosimilar market penetration could reach 45% for targeted therapies.

Here is the catch for patients: Not all biosimilars are designated as "interchangeable." An interchangeable biosimilar can be substituted at the pharmacy without the prescriber’s approval, just like a generic. However, recent FDA guidance has given PBMs confidence to cover non-interchangeable biosimilars anyway. This means your doctor might prescribe Humira, but your plan forces a switch to Amjevita. Many patients report savings of hundreds of dollars monthly with no difference in effectiveness, but others worry about subtle differences in side effects.

If you are switched to a biosimilar, ask your pharmacist: "Is this interchangeable?" and "Are there any known clinical differences I should monitor?" Don't assume they are identical twins; they are close cousins.

How to Spot Changes Before They Hit You

Reactive management leads to skipped doses and financial shock. Proactive management requires checking three specific documents every fall, between October and December.

- The Summary of Benefits (SOB): This high-level overview shows your deductibles and copay tiers. Look for changes in the "Initial Coverage Limit" and "Catastrophic Threshold."

- The Formulary List: This is the master list of covered drugs. Use the online search tool provided by your insurer. Search for every medication you take. Check if it’s still listed and what tier it’s on.

- The Notice of Change (NOC): Insurers are legally required to send this if your coverage changes. It will explicitly state if a drug is being removed, moved to a higher tier, or if new prior authorization requirements apply.

CMS mandates 60-day advance notice for most formulary changes affecting existing medications. However, newly approved generics can be implemented with only 30 days' notice. This is why waiting until January is dangerous. If you see a red flag in November, you have time to act before the new year starts.

Fighting Back: Exceptions, Appeals, and Transitional Supplies

Your drug got kicked off the formulary? Your tier jumped? You aren't powerless. The system has built-in safety valves, though using them requires persistence.

1. Request a Formulary Exception

If your doctor believes a non-covered drug is medically necessary, they can file a standard exception request. In 2024, CMS data showed an 82.3% approval rate for tiering exceptions. However, approvals for completely excluded drugs dropped to 47.1%. To win, your doctor needs to write a Letter of Medical Necessity explaining why the preferred alternative failed or caused adverse reactions.

2. Use Expedited Appeals

If you’re running low on medication and can’t wait, request an expedited review. The insurer must respond within 24 hours. Standard reviews take up to 72 hours. Cigna’s member surveys reveal that while 73% of members successfully obtained exceptions, 38% reported waiting 10-14 days for resolution, causing interruptions. Push for expedited processing if your health is at immediate risk.

3. Leverage Transitional Supply

If you miss the window to appeal or your appeal is denied, you are entitled to a 30-day transitional supply of your old medication. This buys you time to find a new doctor, try a new drug, or gather evidence for an external review. Aetna and other major providers include this provision in their provider bulletins. Ask your pharmacist for this immediately upon receiving bad news.

Looking Ahead: The 2026 Negotiated Drugs

A unique feature of the 2026 landscape is the Medicare Drug Price Negotiation Program (MDPNP) is a federal initiative allowing Medicare to negotiate prices for certain high-cost drugs. Starting January 1, 2026, all Part D formularies must cover negotiated drugs. The first batch includes Stelara (for psoriasis/Crohn's), Prolia (for osteoporosis), and Xolair (for asthma/allergies).

This is a mandatory coverage requirement. Unlike previous years where plans could exclude these drugs, they must now be included. Furthermore, the negotiated prices are required to be at least 25% below current levels. If you take one of these medications, check your plan’s tier assignment for them specifically. They should offer better value than in 2025, but verify the copay amount.

Practical Checklist for Patients

- Review your meds in October: Don't wait for the mail. Log into your insurer’s portal now.

- Identify protected classes: Plan sponsors must cover all drugs in six protected classes (antidepressants, antipsychotics, anticonvulsants, immunosuppressants, HIV/AIDS drugs, and cancer drugs). If your drug falls here, it cannot be excluded, though it can be tiered.

- Talk to your pharmacist: They see formulary changes daily. Ask them, "What is the cheapest therapeutic alternative to my current drug?"

- Document everything: Keep copies of NOCs, exception requests, and doctor notes. If you need an external review later, paper trails win cases.

- Consider Medigap: If you have a Medigap plan (like Plan G or N), it may help cover some Part D costs, but it does not override formulary exclusions. Know your limits.

Navigating formulary updates is frustrating, but it is manageable. By understanding the mechanics of PBMs, the impact of the IRA, and your rights regarding exceptions, you can stay ahead of the curve. Your health shouldn't depend on a spreadsheet update. Take control of the process, advocate for yourself, and ensure your treatment plan remains uninterrupted.

What happens if my drug is excluded from the formulary in 2026?

If your drug is excluded, you have three options: switch to a covered alternative recommended by your doctor, request a formulary exception (which has a ~47% approval rate for exclusions), or use a 30-day transitional supply while you appeal. You can also consider switching Medicare plans during the Annual Enrollment Period (Oct 15 - Dec 7) if another plan covers your medication.

Does the $2,000 out-of-pocket cap include premiums?

No. The $2,000 cap applies only to what you pay for prescriptions (deductibles, copays, and coinsurance). It does not include your monthly Part D premium, Part B premium, or income-related monthly adjustment amounts (IRMAA). Once you spend $2,000 on drugs, the plan pays 100% of covered drug costs for the rest of the year.

Are biosimilars safe compared to brand-name biologics?

Yes, biosimilars are rigorously tested by the FDA to ensure they are highly similar to the reference product with no clinically meaningful differences in safety, purity, or potency. However, because they are large, complex molecules, minor variations can exist. Always discuss potential side effects with your doctor when switching to a biosimilar.

How far in advance will I be notified of formulary changes?

CMS requires insurers to provide at least 60 days' written notice before implementing formulary changes that affect your current medications. For newly approved generics, the notice period can be shortened to 30 days. Check your mail and online account regularly between September and December.

Which drugs are guaranteed to be covered under Medicare Part D?

Plans must cover at least two drugs in each therapeutic category and all drugs in six "protected classes": antidepressants, antipsychotics, anticonvulsants, immunosuppressants, HIV/AIDS treatments, and cancer drugs. Additionally, starting in 2026, plans must cover drugs selected for price negotiation under the MDPNP, such as Stelara and Prolia.